Australia’s mining investment downturn is only about halfway complete, with more pain to come in terms of job losses and the drag on growth.

So says National Australia Bank’s economics team in a new paper that seeks to pinpoint how far we’ve come since the peak of the resources-related capital expenditure boom in 2012.

Demand from China helped drive up commodity prices and encourage mining investment from the early 2000s, allowing Australia and other big resources exporters to weather the global financial crisis in relatively good shape.

However, overcapacity and flatter demand have since pushed prices back down, forcing producers to lift volumes to compensate.

In Australia, new investment in traditional areas such as coal and iron ore is scarce, while development of the country’s liquid natural gas infrastructure is nearing completion.

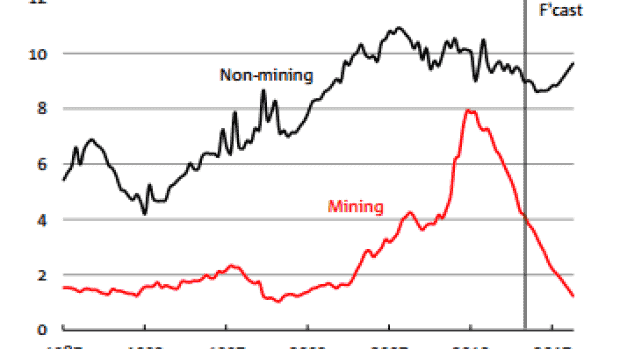

“Our analysis suggests that, given the existing pipeline of mining projects scheduled for completion, the investment downturn is a little over half complete in level terms,” NAB said.

“As a percentage of gross domestic product, mining capex has fallen from 8 per cent at its peak to around 4.5 per cent currently and is expected to fall to 1.5 per cent of GDP by late 2018.”

As the Australian Bureau of Statistics’ quarterly business investment surveys attest, non-mining business investment has been slow to pick up the slack left by the resources downturn, despite record low lending rates.

Economists have ascribed this to a mixture of low expectations for global growth and companies’ focus on shareholder return above productivity-enhancing capital investment.

Rather than invest in new plant and equipment, they argue, companies, particularly in services, are more inclined to hire workers and return excess profits to investors.

In Australia, as elsewhere, this explains falling or steady unemployment rates despite below-trend growth.

Another consideration here, says NAB, is the fact that the resource sector has not been shedding jobs at the rate many had feared.

“So far, the winding down of the mining investment boom has largely unfolded as many had predicted, although the associated fall in direct mining employment has been more muted to date,” NAB said.

“We believe that mining investment is currently more than halfway through the cycle, while employment is slightly below the halfway mark, with the difference likely to be related to the significantly higher labour intensity of LNG projects in the near-completion stage of the construction phase.”

It calculates that 46,000 mining-related jobs were lost between the 2012-13 financial year and last financial year.

It expects another net 50,000 jobs to go over the next two and half years, with 65,000 lost in construction and 15,000 added in mine operations.

However, the bank stresses that jobs growth in other labour-intensive areas of the economy will compensate for the mining downturn in the near term.

“Growth has been particularly concentrated in services sectors which are more labour intensive and in the eastern states, and this pattern is likely to continue,” NAB concludes.

“We expect the unemployment rate to ease gradually to 5.6 per cent by end-2016 [from 5.7 per cent now] and stabilise around that level until end-2017, before inching up in 2018.”